How to protect your portfolio from the coming bear market.

Overpriced Markets

I just finished my review of the year-end results for the Canadian market and I was shocked at the prices I was seeing. You can see long-term charts of average p:e ratios or price to book ratios or graphs of market cap to GDP and they all paint the picture of a market that is in record high territory, but for me, the message really hits home when you go through a long list of companies and you see stock after stock trading at insanely high valuations.

Some sectors are more frothy than others. In the US, the FAANG stocks (Facebook, Apple, Amazon, Netflix and Google) along with a number of other big tech names like Tesla are trading at crazily high valuations eerily reminiscent of the dot com era. In Canada, I’m seeing a proliferation of marijuana and blockchain stocks whose prices simply make no sense.

But this isn’t what frightens me. It’s the run-of-the-mill stock with a completely unremarkable track record of growth and carrying a bit too much debt that is nonetheless routinely trading at a p:e ratio of 20 or more, that has me sweating bullets. In my recent review of the Canadian, small cap marketplace, I found that the average p:e ratio for the typical small cap stock is now sitting at 19.4. In my 21 years of investing, I have never seen this number that high.

While I have done my best to search out what value I can in this overheated market and while the p:e ratios of 10 or 11 that the stocks in my portfolio have look good against the average stock, this is not going to help when the tide goes out. If the market has a big drop then the price of all stocks goes down. In normal circumstances, the average p:e ratio for small caps is 12 and I’ve been able to find good companies selling at 6 or 7 times earnings. Now, with average p:e ratios of 19, I’m finding companies with p:e ratios of 11 or 12. Relatively speaking, I’m still finding the same discounts but when prices start to drop, it will likely affect both the low and the high end of the market and everything in between.

Which means you should be thinking long and hard at this point about your hedging strategy.

Hedging Strategy #1: Cash

There are a few broad hedging strategies that are accessible to regular investors. The first and easiest is to simply cushion your portfolio with a big slug of cash or some sort of “cash equivalent” like a GIC, money market fund or short-term government bond (T-bills).

As I explained in my blog post, “Advice For First Time Investors”, you should always be investing with the mindset that the market could drop in half from where it is today. With prices as high as they are right now, this advice is more relevant than ever. Take a good hard look at your overall portfolio. How much of it do you have exposed to the stock market? Consider the money you have in individual stocks, the money you have in stock-based mutual funds, ETFs, even dividend funds. (Stocks that pay dividends are vulnerable to sell-offs as well.) Are you okay with losing half that money? Figure that out now, not after the market has dropped by 20, 30 or 40%. If you are not, then get the stock part of your portfolio down to a level that does make you comfortable with a 50% loss.

If you’re young and reckless (not a bad thing) then you can afford to take chances. Time is on your side. You may be okay with a 50% loss and you may decide to go in there with guns blazing and be 100% invested in stocks. But if you’ve spent a career building up your nest egg, your risk tolerance is going to be much lower. If you decide that you could handle a 25% drop in the value of your portfolio, then you can achieve this by getting the stock component down to 50% and holding the other 50% in cash or cash equivalents. If a 10% drop in your portfolio’s value would start to make you squeamish then you should really only have 20% of your money invested in stocks and if you think you could weather a 30% downturn then the classic 60/40 weighting between stocks and cash (or low risk bonds) would make sense.

Be careful here not to trade stock market risk for bond risk. With a bond, the basic deal is that you lend someone money and they agree to pay all of it back to you at some point in the future along with some interest along the way. The riskier the borrower is and the longer they have your money before giving it back, the higher the interest they will pay you. The problem now is that overall interest rates are so low (lower than the rate of inflation in many cases) that many investors are unknowingly taking on extra risk to stretch for those higher interest payments. If whatever bond product you are buying comes with a significantly higher interest rate it means that there is very likely some added risk that you won’t actually get all your money back. I would be very careful of bond funds that label themselves “high yield”. There is no free lunch. If these things are offering a higher yield it is because they are investing in riskier bonds that may not pay back in full. When the market starts to drop, it is often the high yield “junk bond” end of the spectrum that runs into trouble first. Buying a high yield bond product is no way to hedge against a market collapse.

So keep your “safe money” safe. Buy a short term GIC from a major bank. Or open up a “high interest” savings account, again at whatever large banking institution you normally bank at. (Not at one of those online-only outfits that raises money with slightly higher interest rates so they can lend it out to riskier “sub-prime” mortgage holders.) If it’s with a major Canadian bank , “high interest” still probably means less than 1% and is about as safe as you’re going to get. A money market fund, provided it is not a “high yield” fund that is pushing itself out on the risk spectrum by mixing dodgy corporate bonds in with its more stable government bonds, is another option.

But honestly, with interest rates as low as they are, just keeping your excess funds sitting in cash in your brokerage account is not the worst idea. This is the option that I choose. The cash is right there when I need it. Yes, it yields 0% but 0% is far, far better than a 50% loss!

So hedging strategy number 1 is to simply own a big chunk of cash. This is going to be the best hedging option for 95% of investors out there. But if you are interested in something a little more aggressive, I have two other ideas, both of which I have employed personally…

Hedging Strategy #2: Hedging with HDGE.

I came across this product a while back and have owned it off and on over the last few years as the market keeps pushing relentlessly higher. HDGE is the ticker symbol for an exchange traded fund called the “AdvisorShares Ranger Equity Bear Fund”. This fund is run by some guys who have been selling stocks short since before the financial crisis of 2008. Selling stocks short means you borrow stocks from someone else, sell them and then hope to buy them back again in the future at a lower price. You then return them to the original owner, pocketing a nice profit for yourself along the way. The managers at the Ranger Bear Equity Fund comb the market, looking for overpriced stocks which they then sell short. They don’t just short the high flying, glamour stocks like Netflix and Tesla, although Netflix has made it onto their short list in the past, they also sell less well-known names that they feel either have questionable accounting or whose fortunes are about to take a turn for the worse. Essentially, they apply a value investing approach to the market, but in reverse. They run a fairly concentrated fund, picking 40 or so of their best ideas at a time. Their picks cover the market and are diversified across market sectors.

The ticker symbol for this fund is HDGE. You can buy HDGE like you buy any other stock so it works well as a way to hedge your stock exposure within a brokerage account. The fund is traded on the US markets, in US dollars and invests in US stocks. As such there will be a bit of a commission charged to convert your money from Canadian into US funds so you can buy the product. As well, if the loonie rises significantly in value against the US dollar then you’ll lose money on the exchange difference, regardless of what the market is doing. This is the major drawback to using this fund as your primary hedging vehicle. While the fund seems to move in reasonably close counterpoint to the direction of the market (going down when the market goes up and going up when the market goes down), if the loonie surges from 78 c to $1.00 against the greenback, then your investment in this US dollar based fund will drop by 28% in Canadian dollar terms. If the loonie drops, then your investment will go up in Canadian dollar terms. So you are taking on some currency risk when you buy this fund.

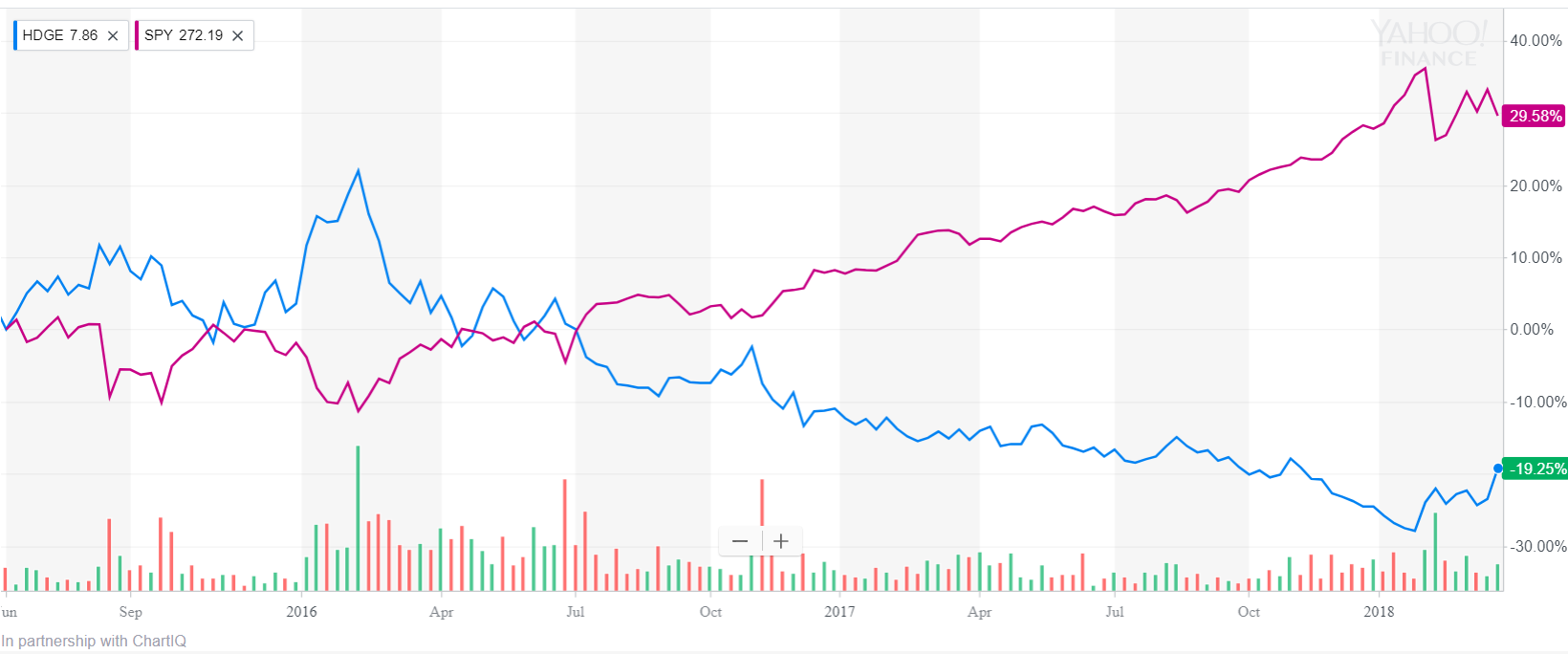

Apart from this, the fund seems to work as it is supposed to. Here is a graph of the fund from just before the market drops in 2015 and 2016 to the present, compared to the S&P 500. (I am using the ETF that tracks the S&P 500 so that it includes the dividend to give a more relevant comparison)

Graph of HDGE (blue) vs. S&P 500 (purple) from 2015 to 2018

As you can see, the fund tracks the inverse of the market reasonably well. Unfortunately we have not seen the fund truly tested by a big, bad bear market. We have had a couple of more minor corrections, though, and the fund performed pretty much as you would hope, rising in value by a similar amount to what the market dropped by. In a longer, drawn out bear market, we can’t be sure of how well the fund’s performance might hold up. To sell stocks short, you first need to borrow the shares to sell. If the market is in a long, drawn-out slump then it could get increasingly expensive to borrow those shares and the cost of shorting could rise, inhibiting performance. On the other hand, the managers of this fund are shorting their best ideas and if they are good at what they do, the names they pick could go down more than the overall market.

At the very least, this fund is highly unlikely to actually lose money in a big bear market and is very likely to make back some, all or even more than what the market loses. So one possible hedging strategy would be to assume that this fund will roughly offset the losses in the “long” part of your stock portfolio. If you decide that you are not comfortable with losing any money at all then you could split your portfolio in two and put half of it into this HDGE fund and buy stocks with the other half. In an ideal world, the gains from the HDGE fund in a bear market would offset the losses in the stock part of your portfolio. However, the same math works the other way around too. Any market gains in the stock part of your portfolio in a normal, rising market would be offset by losses from your HDGE with a net result of zero. You might as well just own cash! Unless you are arrogant enough to think that your stocks are going to outperform the market. If you think that you can beat the market by 5 or 10% then you could hedge out the market risk with this HDGE fund and then hopefully collect the checks on your outperformance and not worry about what the underlying market might do.

For 99.9% of investors this is foolishness. Almost no one beats the market consistently over time. I have, which is why I did at one point in 2015 have almost half of my portfolio in this HDGE product. But for most investors, a smaller allocation to HDGE makes more sense, to partially cushion the blow of a big market downturn. For example, if you put ¼ of your portfolio into this HDGE then, if its performance was an exact reverse mirror of the market and the market dropped by 50%, the part of your portfolio that you had in stocks would drop in half while the smaller allocation to HDGE would go up by 50% and when the dust settled you’d have lost 25% overall.

You can think of this as cash on steroids. For most investors, simple cash is the better option. With this HDGE fund, there is the added currency risk as well as the chance that the fund may not move in the opposite direction of the specific stocks you own. (Maybe Canadian stocks will go down while US stocks continue to move up which would mean you would lose money on both your long stock holdings as well as on your HDGE position. Ouch!)

I mention the fund here because it is something that I have used and have found helpful in the past. I can see it being useful in the case of someone who is new to investing in individual stocks and is keen to try their hand at this “game” but is nervous about the current overall level of the market. They could decide to sit on the sidelines and wait until prices dropped before getting in, but they could be waiting years. Timing the market is very difficult. I have been hedging off and on since 2015. Instead of waiting for the optimal time to invest, perhaps they could buy a basket of stocks and then offset that risk at least partially by buying some of this HDGE fund as well.

NOTE: There are a bewildering number of “inverse ETFs” out there that promise to offer this same sort of hedging behaviour, going up in price when the market drops and vice versa. You need to be very careful with these. Most of them use derivatives like futures contracts and options to make bets on market direction and these derivative products can be expensive and unpredictable. Especially when you’re dealing with the 2x or 3x versions of these inverse ETFs, that use various derivative strategies to magnify the underlying movements of the stock market, you may not get the results you are expecting. If you hold them for longer periods of time, their performance can dramatically underperform the inverse of their benchmark index. I like the HDGE product because it doesn’t mess around with this stuff; it invests in actual, individual companies by selling them short and applies a fundamental, reverse-value oriented approach.

Hedging Strategy # 3: Put Options

I will only mention this strategy because it is the one that I am currently employing. Namely, buying put options on one of the major indexes. Buying options is a very risky and dangerous game. If you don’t know what you’re doing it could blow a big hole in your portfolio. Please do not attempt this unless you already have experience trading options. For those without this experience and especially for investors who are relatively new to the game, stick with using a healthy cash buffer or, if you are a little more adventurous you could seek out a fund like the Ranger Equity Bear Fund that sells stocks short. Skip the explanation below and move on to hedging strategy number 4.

But for those of you who already have experience trading options, here’s the strategy I’m employing right now: Back in early January, I bought 1 year put options on an exchange traded fund that tracks the S&P 500. (ticker symbol: SPY). I chose this as my target because it is very heavily traded and the options on this ETF are also very heavily traded. There is lots of volume, so I can get in and out when I want. I tried looking at options for individual Canadian stocks and found the volume low and the selection very limited. Options on a big, Canadian ETF might have been an option, but I’ve found the US indexes to be a better benchmark for my own portfolio than the Canadian ones because the Canadian ones are so heavily exposed to the resource industry and the big banks. I tend to avoid both. Finally, I went with the S&P 500 as my target instead of the smaller cap Russell 2000 because I have accumulated extensive historical data on the S&P 500 and have a much better idea of where this index stands, valuation-wise, relative to its historical record. I can update this data on a regular basis and have more confidence that I have a good read on where its price is relative to historic norms. Some of the most egregious cases of overvaluation right now are in the big tech names that are included in this index. And finally, the options you can buy to hedge against a given percentage of downside risk are significantly cheaper for the S&P 500 than they are for the Russell 2000. (Whereas I feel the downside risk for both is similar.)

Once I identified my target, I went through multiple scenarios, plugging them all into a spreadsheet. The strategy I came up with was to buy 1 year, “in the money” put options on the S&P 500 (or rather the SPY ETF that is tied to this index). My plan is to roll over these put options just before they are due to expire (ie sell the options) and buy a new batch of 1 year options that are again just slightly in the money at that point. I’ll continue doing this as long as the option pricing seems reasonable and as long as I remain terrified of a major market drop.

My rough calculations go like this: I am buying put options that are 5% in the money. In early January, I bought SPY Put options at 290 expiring Dec 21 of 2018 when the S&P 500 was at 2750 and the SPY ETF that tracks this index was at 275. I paid about 10% of the strike price for these options (ie $29 in Canadian dollars). If the S&P 500 ends the year up more than 5% then I would lose this entire investment. But if it closes down 10% then I stand to roughly double my money on this investment. If it closes down 20%, I triple my money and if it closes down 30%, I quadruple my money.

If I put around 10% of my portfolio into this strategy every year then the gains in my put options should cancel out any losses in my stock portfolio, assuming that my stocks do not drop more than the S&P 500 (which may not be a safe assumption given the kind of beaten up, small cap stocks I like to buy).

If the market waffles sideways or worse, keeps rising, then at least I still have the bulk of my portfolio invested in stocks. If I was not outperforming the market, the 10% I’d be losing every year on my put options in a rising market would be a real kick in the teeth and would make this strategy more or less untenable. I’m operating on the assumption that I can continue to beat the market (in a rising market at least) by 13% or more per year, as I have for the past 20+ years. In this scenario, I can still hopefully make money, even with the significant drag from the put options, but it would be significantly less than what I might have made if I wasn’t such a chicken little.

Hedging Strategy #4: The Best Defense Is A Good Offense

Whatever hedging strategy you choose, it won’t be perfect. There are no guarantees in life and certainly no guarantees in the stock market. The market has a way of doing the complete opposite of what you expect it to. It could well be that a portfolio put together from a carefully chosen basket of undervalued stocks is going to outperform any elaborate hedging strategy you might come up with. This would be especially true if the market just drifts sideways for many years as it might well do. In this scenario, the best defense is going to be a good offense. With prices where they are now a very realistic expectation is for stocks (and bonds) to return close to zero percent over the next decade or two. If there is no great crash but just a long, sideways wheeze then the best strategy is going to be to search out undervalued, overlooked bargains and hope that you can beat the 0% market return.

That is why, even with the high prices I am seeing, I am still aggressively invested with most of my portfolio in a basket of hand-picked, value priced stocks. I do have put options to protect myself from a major drop and I think most investors would be well advised to have some significant cash set aside to cushion a major market blow-out, but for the money that you commit to the market, taking the time and effort to research and choose individual names for your portfolio that you know offer good value, could end up paying the biggest dividends.